Last Mile-Peak Season Updates

The last-mile supply chain is in full swing as the holiday season rapidly approaches. While historically, Black Friday was the pinnacle shopping day of the year, retailers have increasingly extended the holiday shopping season to nearly two full weeks of sales. Black Friday sales now often commence as early as Wednesday, and Cyber Week sales extend through the week after Thanksgiving. As these two weeks involve heavy volumes for retailers, assessing how their performance is can help set the tone for how the rest of peak season will proceed.

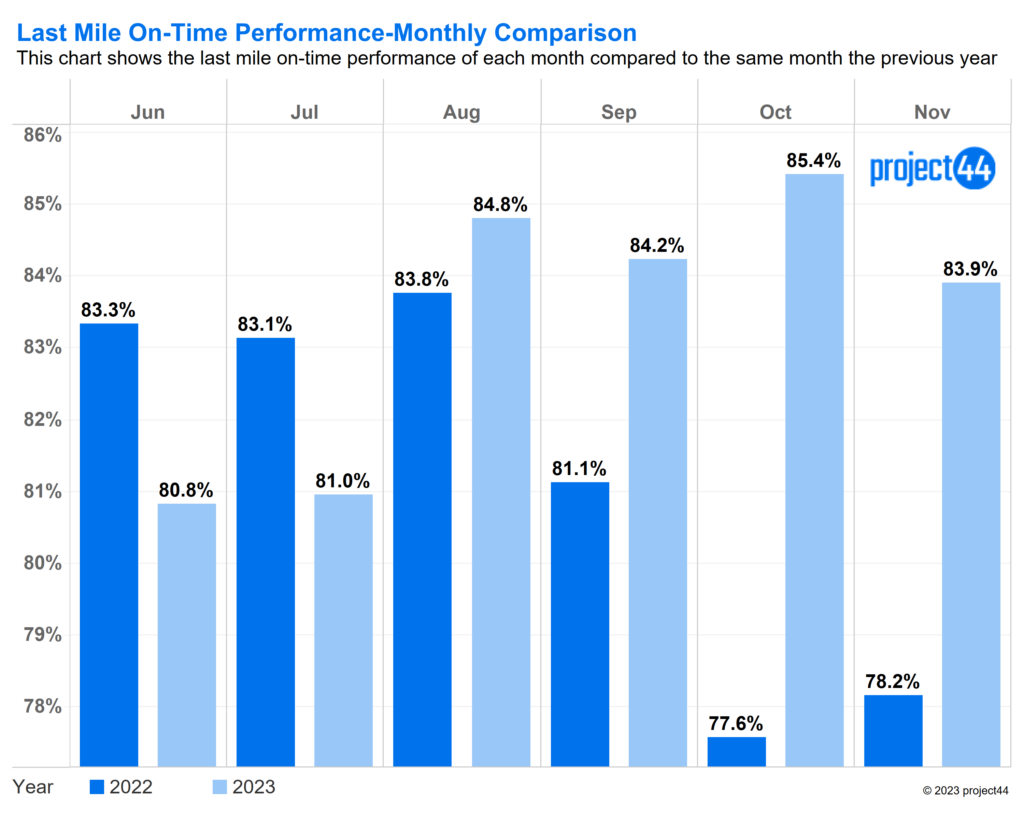

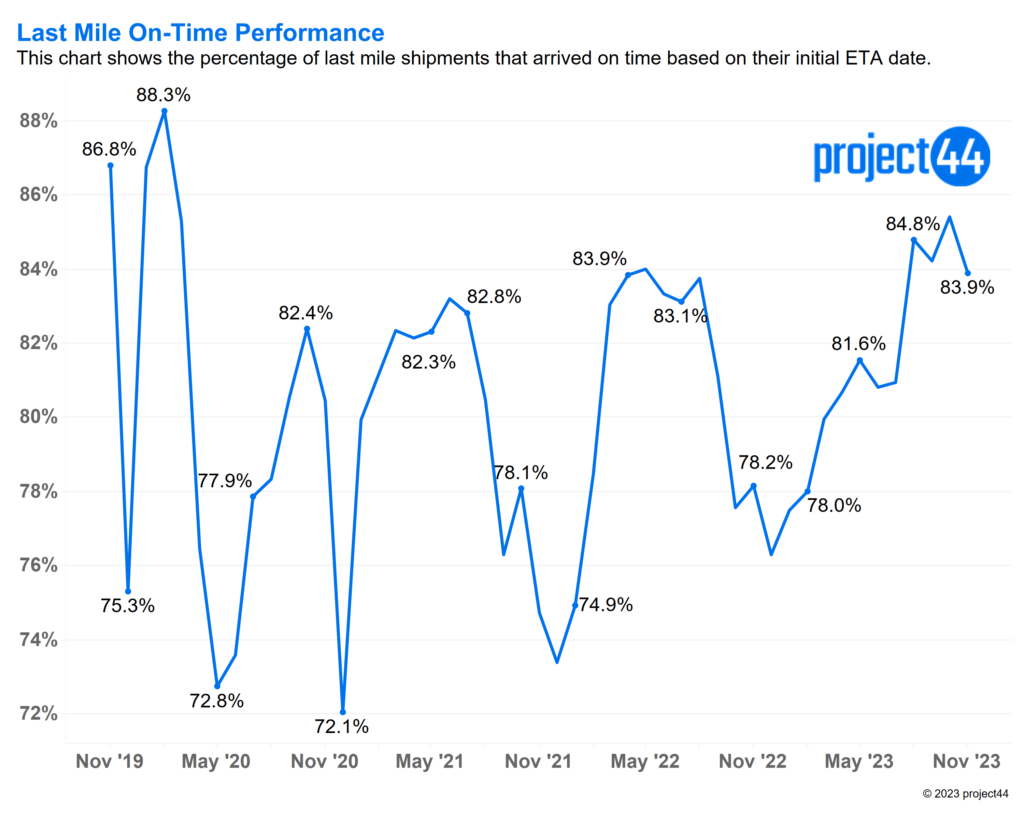

On-Time Performance

On-time performance typically experiences an annual dip in the months of November, December, and January, and this peak season is no exception, as illustrated in the chart below.

Between October and November, there was a 1.5% decrease in on-time performance, expected to further decrease in December. Despite the decrease from October, November 2023 is trending 5.7% higher than 2022 for on-time performance. With volumes comparable to last year, this difference highlights the overall health of the market in 2023.

Comparing the current peak season over a more extended period, November 2023 represents the best on-time performance since pre-Covid19. November of 2019 narrowly surpassed 2023 by a mere 2.9%.

One interesting thing to note is that so far in 2023, peak season is outperforming the rest-of-year average of 81.9%. This level of performance has not been seen since the 2020 peak season, which had the beginning of the pandemic factored into the average, bringing it down. 2023 has been witnessing significant improvement in on-time performance throughout the year.

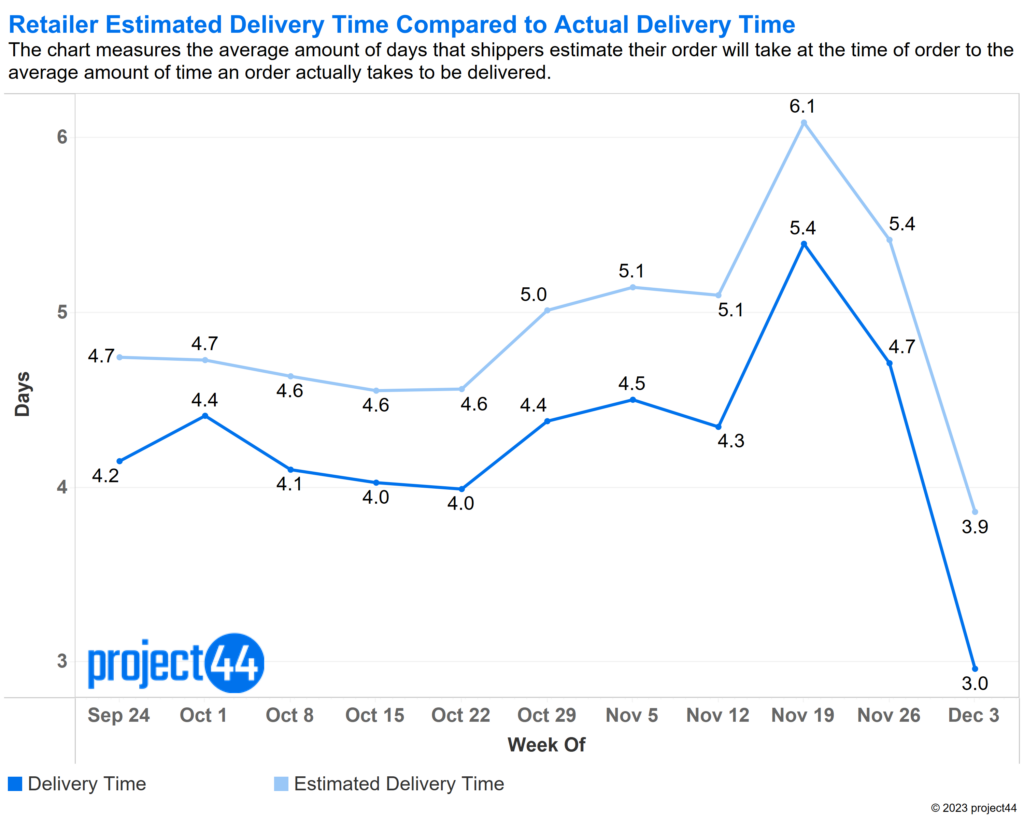

Estimated Delivery Time Compared to Actual Delivery Time

To prepare for the impacts of increased peak season volume on fulfillment and transit times, retailers often increase their estimated delivery times provided to customers at the time of order placement.

As the weekly breakdown shows, the week of November 19th, which kicked off Black Friday sales this year, saw a one-day increase in estimated delivery times, a 19.6% increase from the previous week. This decision on the retail side proved beneficial, as there was a 25% increase in delivery time between the weeks of November 12th and 19th. The additional padding in estimates meant that, despite a larger increase in delivery times, packages, on average, were still delivered prior to their estimated delivery date.

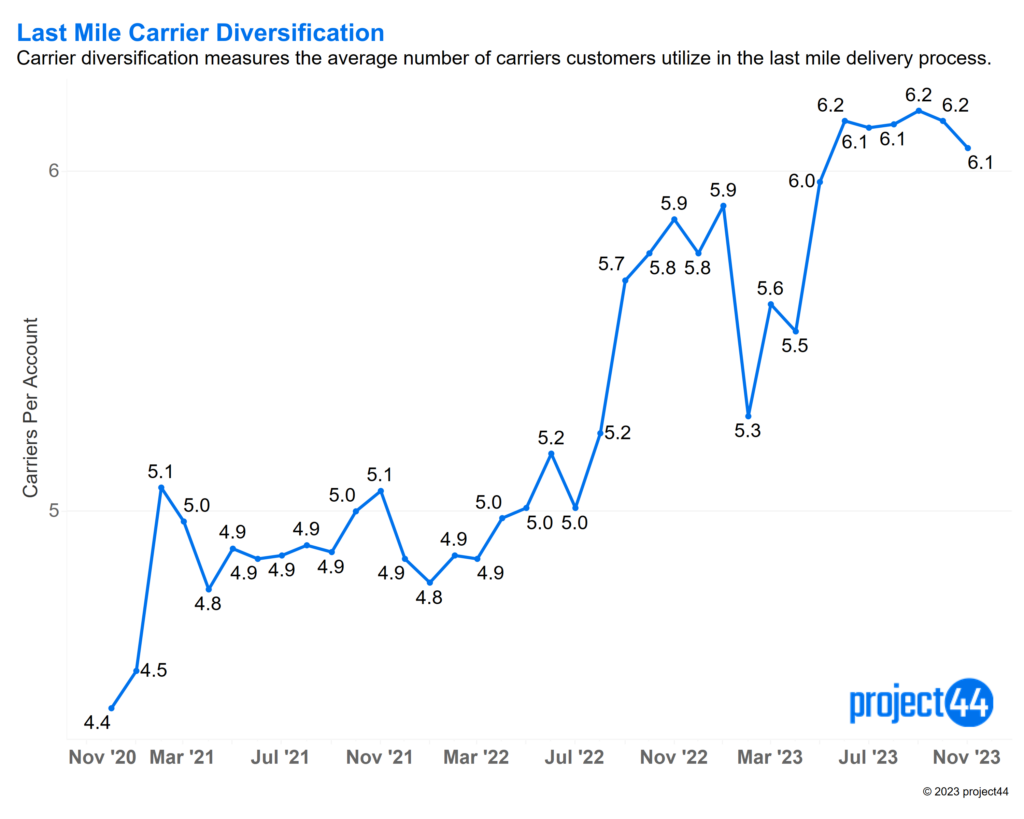

Carrier Diversification

As mentioned in previous reports, carrier diversification saw an early increase this year due to the threat of strikes by UPS. In 2022, retailers began increasing the number of carriers used to handle outbound shipments in September. This year, the jump occurred in May, a full four months earlier.

Since the jump in September, the average number of carriers retailers are using has remained steady, plateauing around 6.1 carriers. It is anticipated that this number will stay stable through the peak season and then begin to decrease after January.

Outlook

Peak season 2023 is off to a strong start. Despite a small decrease in on-time performance and an increase in delivery time, 2023 is shaping up to be the top-performing peak season since the pandemic.

For questions or comments:

press@project44.com

Disclaimer: The information conveyed herein, shared solely for summary and not contractual purposes, comes from both project44 and third-party reporting. The project44 data does not include all available market information, and project44 has not undertaken to independently verify the third-party reporting. Similarly, this type of data changes from day-to-day. Accordingly, the reader should not rely on this reporting to make any business decisions, and project44 expressly disavows any liability arising from any such reliance.