Summary:

- On-Time Performance continues to lag behind 2022 but is trending upwards for 2023. This is partially driven by an increase in volume in 2023.

- Promise and Delivery times continue trending down, with the lowest estimates and delivery times recorded seen in July.

- Carrier diversification saw an unprecedented uptick in June and July, likely due to the threat of the averted UPS strike.

- The most common customer complaints continue to be package delays and delivered but missing packages, which can be mitigated through visibility and proactive communication to customers.

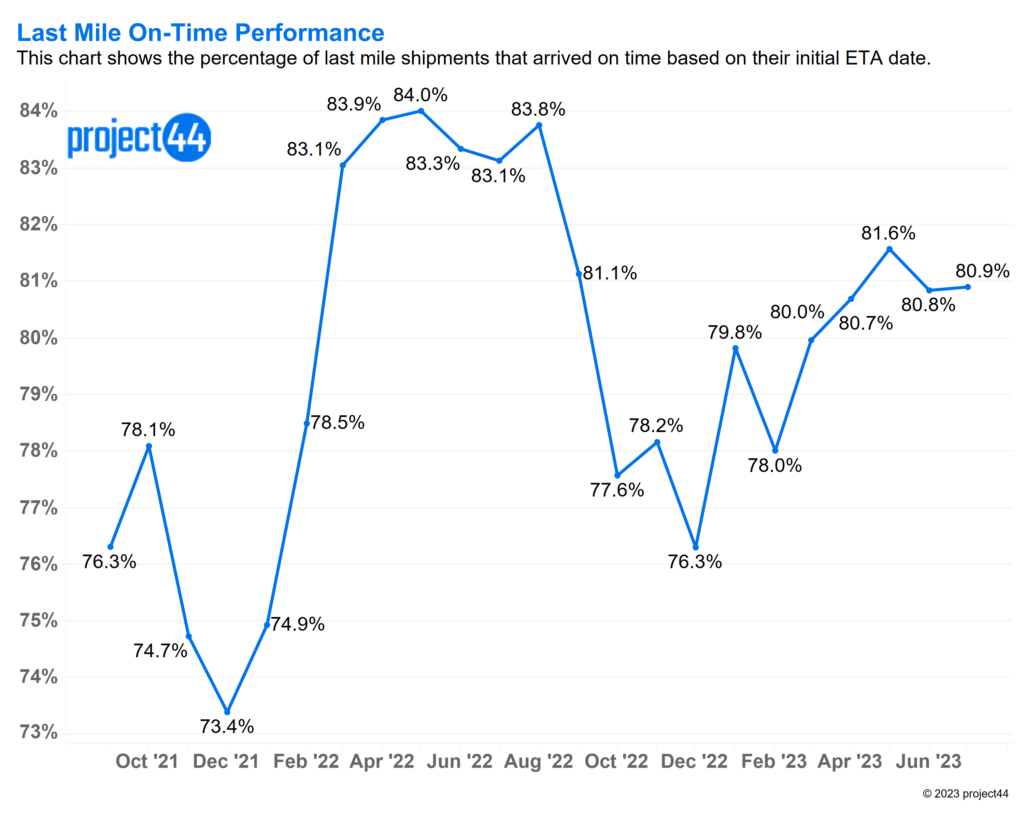

On-Time Performance Trends

Based on project44 data, July 2023 is currently trending 2.2% lower compared to July 2022. Throughout 2022, there has been a consistent pattern of outperformance when compared to 2023, a trend that has persisted since February. However, it’s important to note that one influential factor behind this divergence could be the noticeable uptick in volume observed in 2023. Specifically, July 2023 boasts a 4.4% increase in volume in comparison to the same period in 2022.

Longer-term trends consistently emphasize that 2023 has not been able to match the service standards set by 2022. However, there has been a promising upward trend in 2023 that we will hopefully continue to see, especially now that the threat of a looming strike from UPS workers has dissipated. We are seeing a nearly 3% improvement in July compared to the annual lowest performing month of February, which was a low of 78% on-time performance. Should this trend continue, it puts the market in a good place going into peak season.

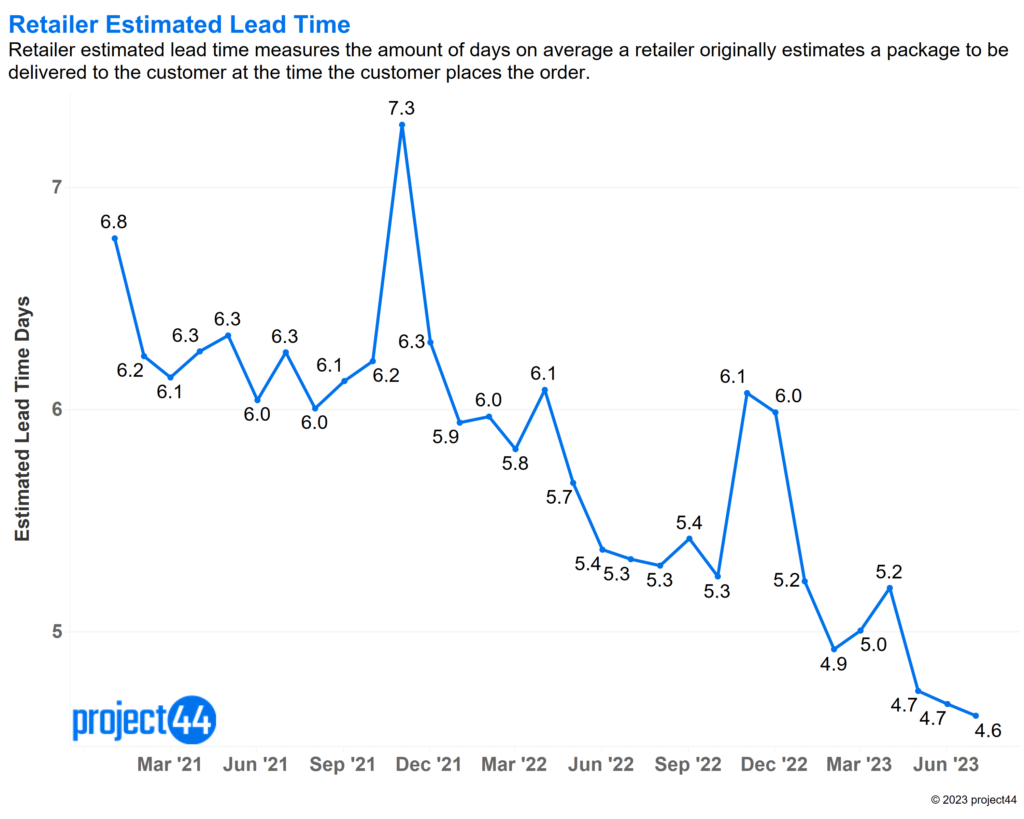

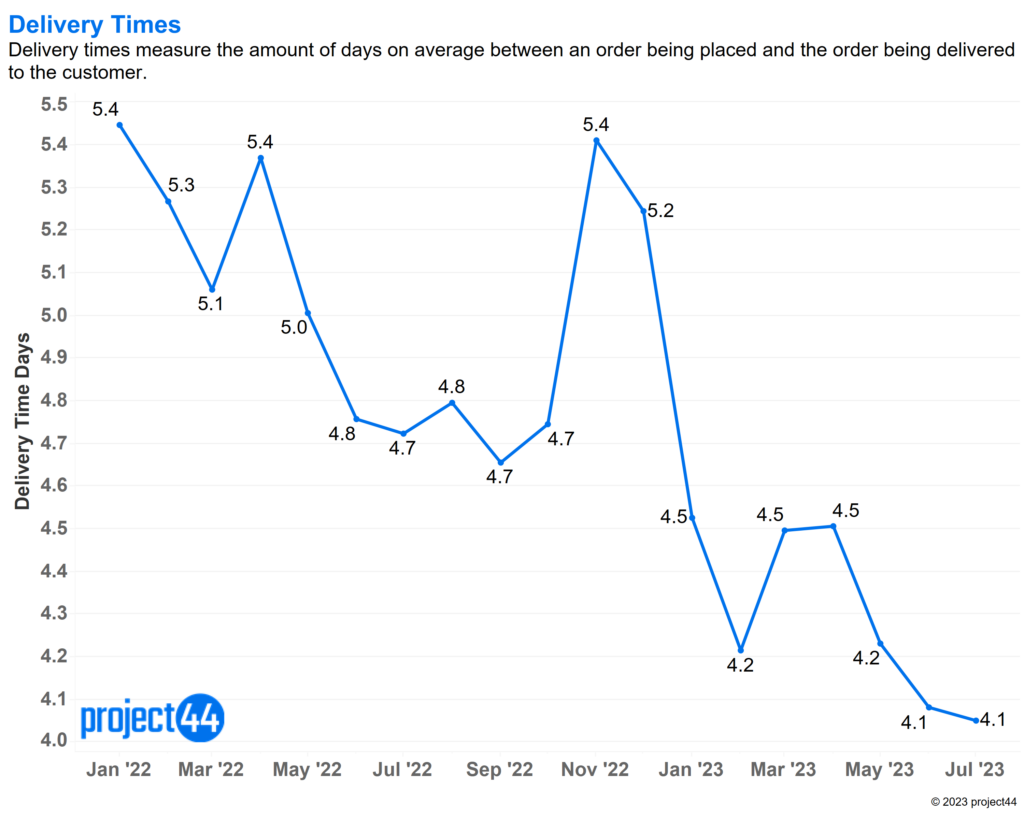

Promise and Delivery Time Trends

Time estimates from retailers continue to decrease with July marking a new low of 4.6 days from the time the order is placed. This number has previously hovered close to 1 week, showing the demand for faster delivery times in a changing ecommerce landscape, as well as a shift in confidence from retailers that they can process and ship goods more efficiently. Retailer operations and locations have had to shift strategically to make this happen.

The chart below clearly illustrates how the investments companies have made to enhance their shipping times are yielding positive outcomes. The actual average delivery time stands a solid half-day lower than the initially promised timeframe, coming in at just 4.1 days. A range of effective strategies have been put into action to achieve these notable results:

- Introduction of automated warehouse processes, such as mech lines, has enabled facilities to efficiently handle more goods within the same time frame, ensuring heightened accuracy.

- Retailers have strategically invested in real estate to establish distribution centers at optimal locations, thereby shortening transit times across the United States.

- A focus on diversifying carrier options and forging stronger partnerships with carriers has empowered retailers to efficiently meet the increasing product demands while minimizing potential delays.

Carrier Diversification Trends

June and July have revealed peaks in carrier diversification. Typically, these months aren’t known for sudden spikes in diversification; that tendency usually emerges around August and September as retailers gear up for the busy holiday season. However, this year’s unusual trend could directly stem from the looming threat of a UPS strike.

UPS holds a dominant position in the last-mile delivery sector, and it narrowly dodged a strike involving over 300,000 workers at the end of July. Such a strike could have wreaked havoc on the last-mile market. To hedge against this risk, numerous retailers took steps to bring other carriers on board, reducing their reliance on UPS. Even though the UPS strike was ultimately averted through a labor agreement, the mere possibility of such a massive disruption can alter market dynamics and affect the allocation of volume to the potentially affected carrier.

Customer Complaints

The primary customer complaints persist in the last-mile market, where delays and cases of delivered but missing packages together account for more than half of the reported issues. Occasionally, delays are unavoidable, particularly in the wake of recent severe storms and flooding that affected certain parts of the US this summer. However, retailers do possess means to enhance customer satisfaction by proactively addressing delays through real-time updates on package statuses. While some customers might still experience frustration, the sooner they are informed about a delay, the more time they have to arrange for alternatives, especially if the package is urgent.

Real-time alerts can also help mitigate instances of delivered but missing packages, which often result from theft. Frequently referred to as “porch pirates,” thieves specifically target packages left unattended on doorsteps. The deployment of delivery alerts can substantially reduce the duration during which a package remains unattended, thus lowering the likelihood of it being snatched by these opportunistic thieves.

Overview

The last mile market remains relatively stable on the whole. Although on-time performance rates have dipped compared to previous years, they currently stand at 80%, and packages are being delivered faster on average than ever before. The market encountered a significant challenge with the near UPS strike, a situation that was fortunately averted. Despite the avoidance of the strike, there is still a discernible uptick in carrier diversification, indicating that retailers are taking proactive measures in response to potential risks. Anticipate this trend of diversification to continue its upward trajectory, particularly as the peak season approaches.